The Overseas Owner's Guide to Selling Japanese Real Estate ─ 5 Sale Methods Worth Knowing

This comprehensive guide explains the 5 primary methods by which non-resident owners can sell Japanese real estate, based on Japan MLIT's November 2025 data and industry observations. Of 308 units acquired by overseas residents in Tokyo's 23 Wards, Taiwan accounted for 192 units (over 62%). Covers the 10.21% withholding tax, capital gains tax rates (30.63% short-term, 15.315% long-term for non-residents), the 30-million-yen special deduction applicable to former residences, and the April 2026 FE

── 5 Sale Methods Worth Knowing, Even If Long-Term Holding Is Your Plan ──

📋 Article Summary

This article compares methods of selling. If you are keeping the property and renting it out instead, see Owning a Japanese home while living abroad for withholding tax and tax representatives.

This article systematically explains the 5 primary methods by which overseas-resident owners (non-residents under Japanese tax law) can sell Japanese real estate, based on the latest data from Japan's Ministry of Land, Infrastructure, Transport and Tourism (MLIT) published November 25, 2025, and on practical industry observations.

Key Points:

- Of 308 units acquired by overseas residents in Tokyo's 23 Wards, Taiwan accounted for 192 units (over 62%) — the dominant majority

- The 10.21% withholding tax is paid directly by the buyer to the tax office — a system unique to Japan

- Capital gains tax rates for non-residents: 30.63% income tax (short-term, ≤5 years), 15.315% income tax (long-term, >5 years). Resident tax generally does not apply to non-residents.

- The 30-million-yen special deduction can apply to a former personal residence if sold by December 31 of the third year after departure (NTA No. 3314)

- The April 1, 2026 FEFTA ministerial ordinance amendment makes all non-resident transactions subject to 20-day post-transaction reporting

5 Sale Methods with Estimated Shares:

- Direct sale to professional buy-and-resell operators (40–50%)

- Standard real estate brokerage (30–40%)

- Multilingual / foreign-capital brokerages (10–15%)

- Direct transactions between foreigners (5–10%)

- Transfer via inheritance / gift (5–15%)

About the Author

Joji Uramatsu

- Former Bureau Chief, Mainichi Shimbun China Bureau (3 years stationed in Beijing; studied at National Taiwan Normal University; 34 years as a journalist and editorial desk)

- Triple-licensed: Administrative Scrivener (Gyoseishoshi), Labor and Social Security Attorney (Sharoshi), Licensed Real Estate Broker (Takken-shi) — all passed on the first attempt

- Representative Director, Yotsuba Real Estate Co., Ltd.

- Principal Administrative Scrivener, Yotsuba Administrative Scrivener Office

- Operator, Shigyo.com SAMURAI

- Native-level proficiency in Chinese (both Traditional and Simplified)

Introduction: Why "Knowledge for When the Time Comes" Matters

For overseas residents who own real estate in Japan, the property is, in most cases, a valuable asset held with the assumption of long-term ownership.

As a yen-denominated asset for value preservation, as housing for children studying in Japan, as preparation for future relocation to Japan, as a family second home, or as an investment property generating stable rental income — the purposes of holding are diverse.

Yet life brings unexpected turning points. Family circumstances, the occurrence of inheritance, capital needs in your home country, changes to your life plan — the day may come when you consider selling.

When that day arrives, you should be able to make the optimal decision without panic. This column is not a call to sell. We hope you read it as "knowledge for when the time comes."

Q1. What Is the Current State of Overseas Acquisition of Japanese Real Estate?

MLIT's First-Ever Comprehensive Survey

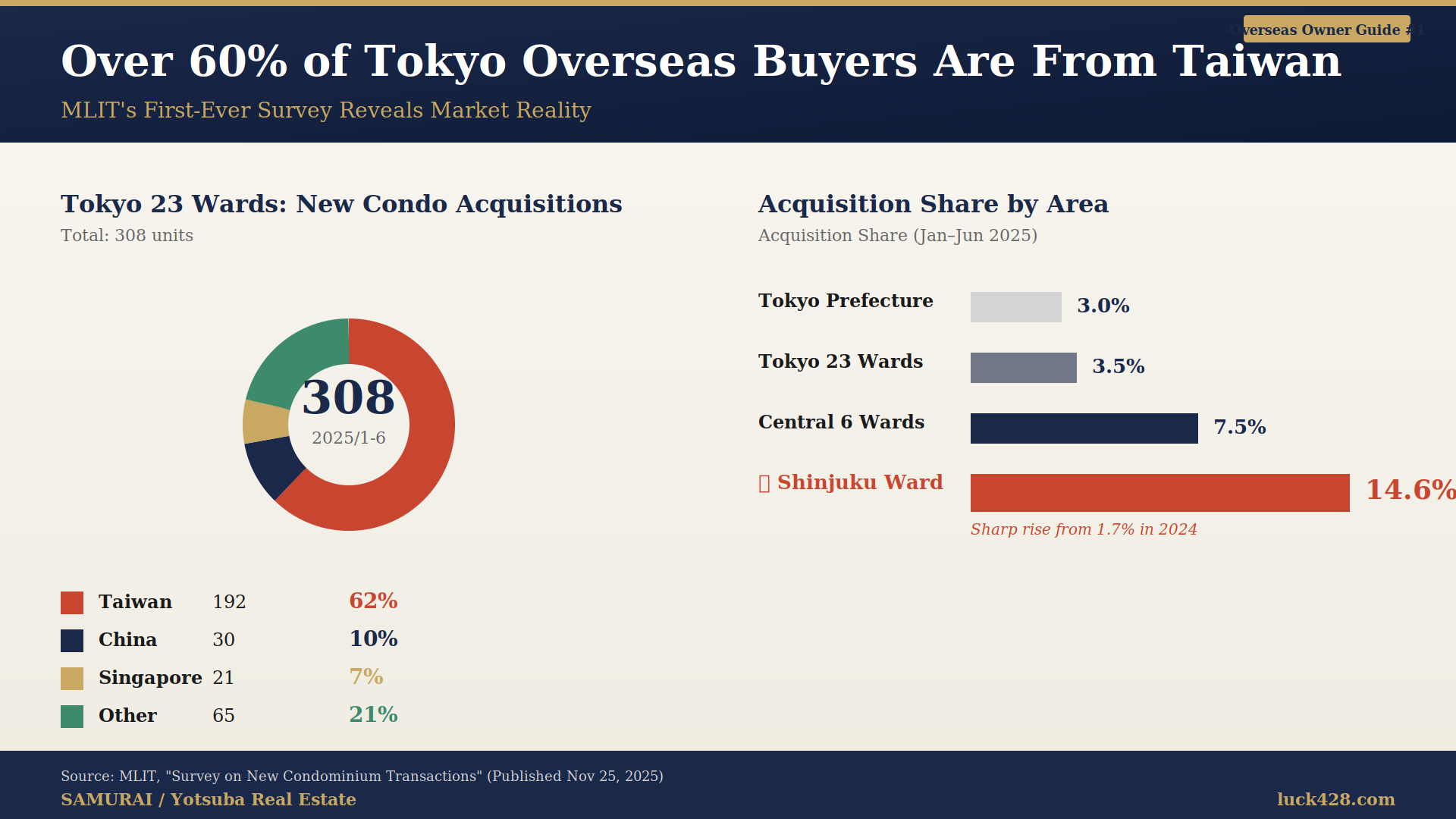

On November 25, 2025, Japan's Ministry of Land, Infrastructure, Transport and Tourism (MLIT) published "Survey Results on New Condominium Transactions Using Real Estate Registration Information" — the first full-scale governmental survey of this nature.

Survey Overview:

| Item | Details |

|---|---|

| Publication Date | November 25, 2025 |

| Survey Period | January 2018 – June 2025 |

| Survey Scope | ~550,000 new condominium units in 3 major metropolitan areas + 4 regional cities |

| Data Sources | MOJ real estate registration data + private price data |

Key Data for January–June 2025

| Area | Overseas Resident Acquisition Share |

|---|---|

| Tokyo (entire prefecture) | 3.0% |

| Tokyo 23 Wards | 3.5% |

| Central 6 Wards (Chiyoda, Chuo, Minato, Shinjuku, Bunkyo, Shibuya) | 7.5% |

| Shinjuku Ward (notable) | 14.6% (sharp rise from 1.7% in 2024) |

| Osaka City | 4.3% |

| Kyoto City | 2.5% |

Acquisition by Country/Region (Tokyo 23 Wards, Jan–Jun 2025)

Of 308 units acquired by overseas residents in Tokyo's 23 Wards:

| Country/Region | Units | Share |

|---|---|---|

| Taiwan | 192 units | Over 62% |

| China | 30 units | ~10% |

| Singapore | 21 units | ~7% |

| Other | 65 units | ~21% |

This indicates that investors from the Greater China region, with Taiwan at the center, form the principal demographic of overseas owners in Japan's real estate market.

Q2. What Are the Most Important Facts Before a Non-Resident Sells Japanese Real Estate?

There are 4 essential facts every non-resident must know before selling Japanese real estate.

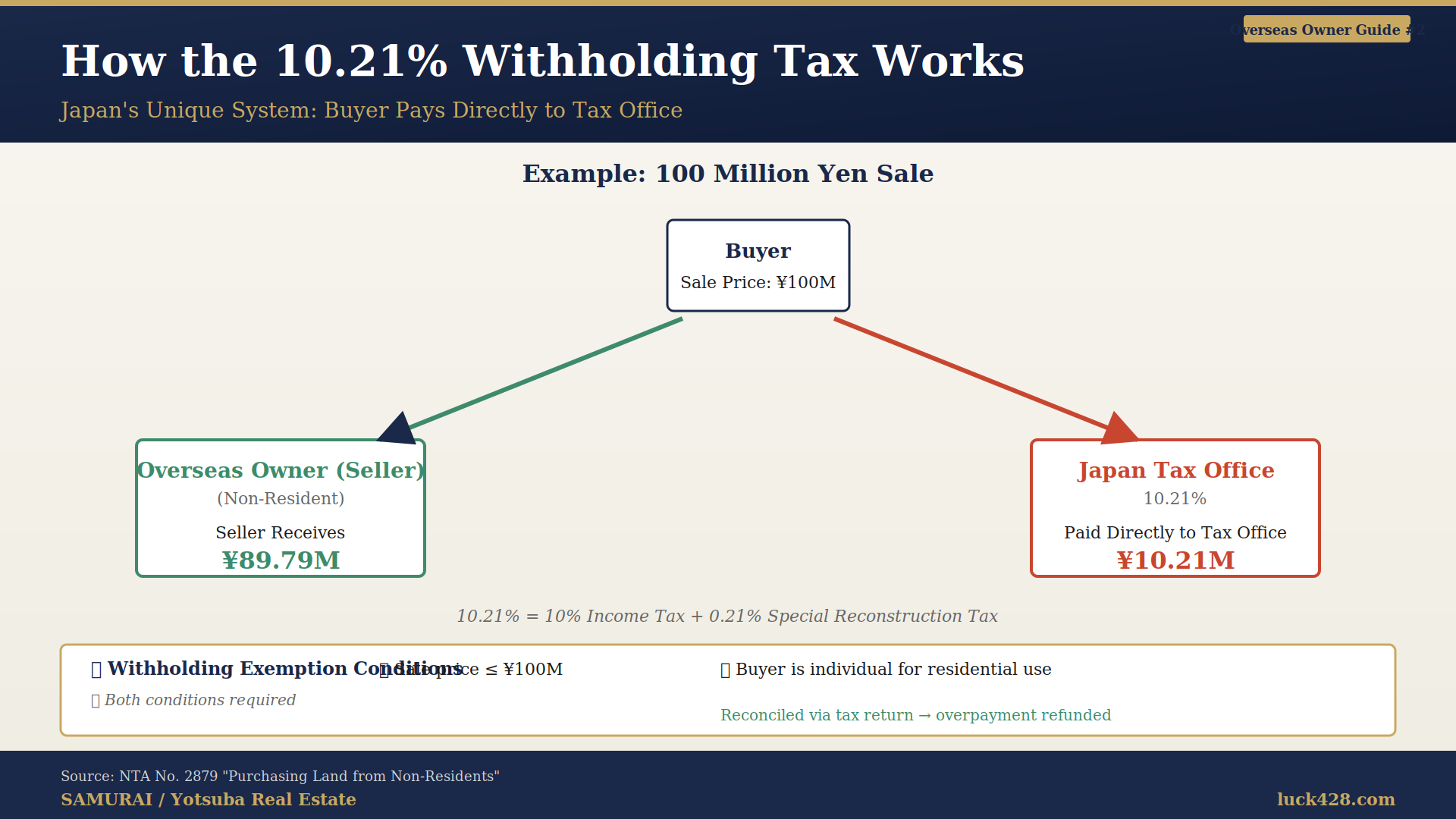

Fact 1: Japan's Unique 10.21% Withholding Tax System

When a non-resident sells Japanese real estate, the buyer is obligated to withhold 10.21% of the sale proceeds and remit it directly to the tax office.

Note that 10.21% applies to sale proceeds, while 20.42% applies to rent — different rates under different provisions. The two are easily confused.

| Item | Details |

|---|---|

| Tax Rate | 10.21% (10% income tax + 0.21% special reconstruction income tax) |

| Payer | The buyer (not the seller) |

| Payment Deadline | By the 10th of the month following payment |

| Legal Basis | Income Tax Act Articles 161 & 212; Reconstruction Finance Act Article 28 (NTA No. 2879) |

Example: 100 million yen sale

- Amount received by seller from buyer: 89.79 million yen

- Amount paid by buyer directly to tax office: 10.21 million yen

Exemption Conditions (both must be met):

- Sale price is 100 million yen or less

- Buyer is an individual purchasing for residential use by themselves or their family

Fact 2: Tax Return Filing Is Mandatory

Even non-residents are subject to Japanese capital gains tax on profits from selling Japanese real estate.

Non-Resident Capital Gains Tax Rates (excluding resident tax):

| Category | Rate | Breakdown |

|---|---|---|

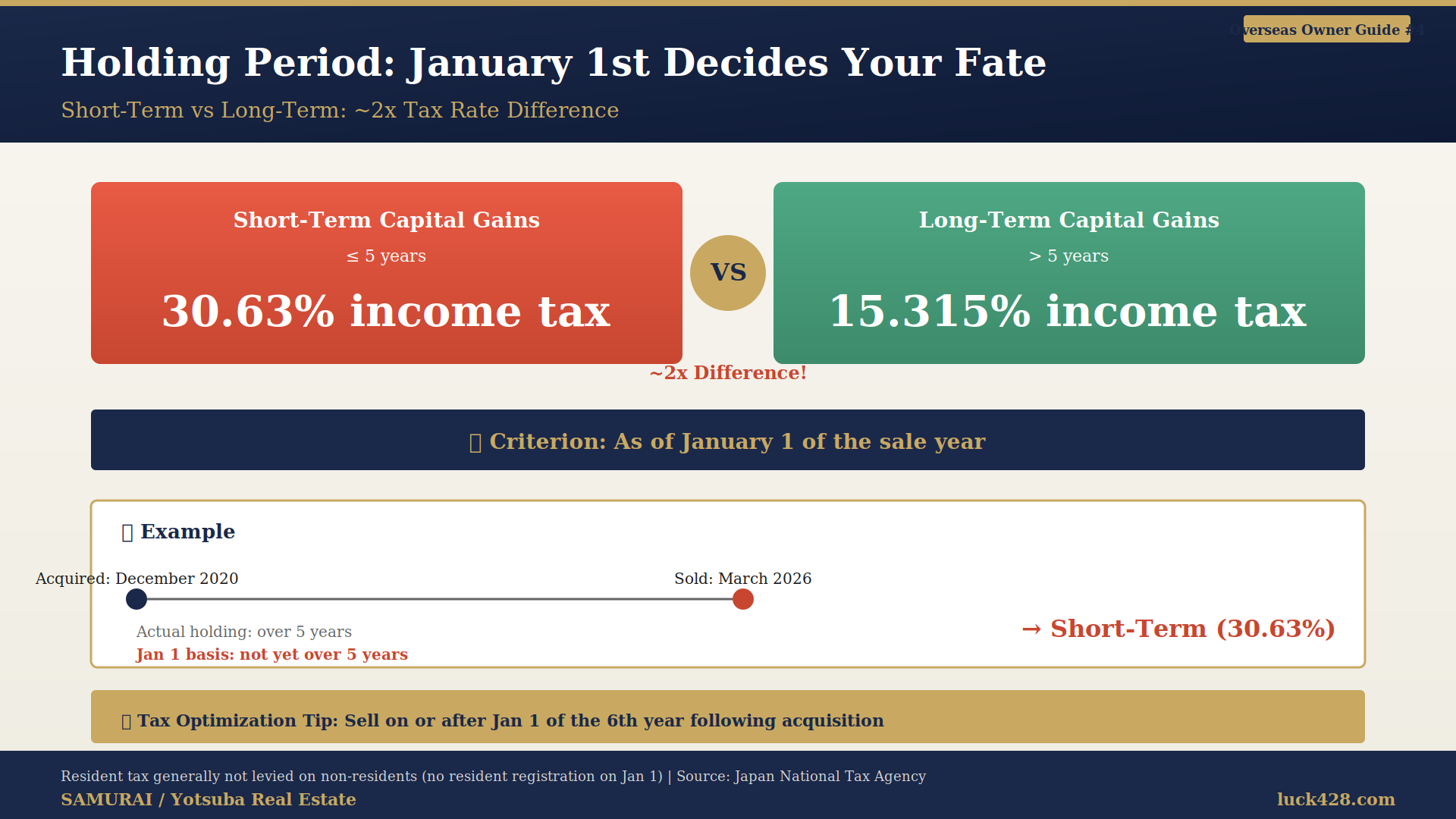

| Short-term (held ≤5 years) | 30.63% income tax | 30% income tax + 0.63% special reconstruction income tax |

| Long-term (held >5 years) | 15.315% income tax | 15% income tax + 0.315% special reconstruction income tax |

Important Notes:

- Resident tax (inhabitant tax) generally does not apply to non-residents

- However, if you still have a Japanese resident registration as of January 1 of the sale year, resident tax (9% short-term, 5% long-term) is additionally levied

- Tax filing period: February 16 – March 15 of the year following the sale

- The 10.21% withheld is reconciled through the tax filing (overpayments are refunded)

Critical Note on Holding Period Determination:

The criterion is "whether the holding period exceeds 5 years as of January 1 of the sale year."

Example: A property acquired in December 2020 and sold in March 2026 has an actual holding period of over 5 years, but as of January 1, 2026, it has not yet exceeded 5 years — so it is treated as short-term capital gains. To qualify for long-term rates, you must sell on or after January 1 of the sixth full calendar year following acquisition.

Fact 3: Japan-Specific Documentation Is Required

Standard Japanese real estate sales require a Resident Card (Juminhyo) and a Registered Seal Certificate (Inkan-shomeisho), but these are not issued to overseas residents.

Substitute Documents (obtained at the Japanese embassy/consulate in your country of residence):

- Certificate of Residence (Zairyu Shomeisho) — substitute for Juminhyo

- Signature Certificate (Shomei Shomeisho) — substitute for the Registered Seal Certificate

Obtaining these typically requires 2–4 weeks, including embassy appointment and in-person visit.

Fact 4: Appointing a Tax Representative Is Effectively Mandatory

For non-residents who cannot use Japan's e-Tax system, appointing a Tax Representative (Nozei Kanrinin) is effectively mandatory for tax filing procedures.

A Tax Representative acts as the point of contact with the tax office for a person who has neither a domicile nor a residence in Japan (Act on General Rules for National Taxes, Article 117).

There is no professional qualification requirement to serve as a Tax Representative. However, preparing and filing tax documents — such as a tax return or the notification of a Tax Representative — and acting as a tax agent are the work of a licensed tax accountant (Zeirishi) (Certified Public Tax Accountant Act, Article 2(1)(i) and (ii); Article 52). Even where a service offers to "act as your Tax Representative," check separately whether that includes preparing tax documents.

Who to ask (when selling):

| Option | Suits you if | Points to weigh |

|---|---|---|

| A tax accountant (Zeirishi) | You are selling and must file capital gains | Filing fees apply; managing the property itself is out of scope |

| A family member in Japan | Mainly receiving documents from the tax office | No qualification requirement, but a family member cannot prepare the tax return either (Certified Public Tax Accountant Act) |

| Yotsuba Real Estate + partner tax accountant | Your property is in or near Bunkyo Ward and you are still deciding whether to sell | Brokerage and document handling by Yotsuba Real Estate; filing under a separate, direct contract with the partner tax accountant. No referral fees are exchanged |

If you plan to keep and rent out the property rather than sell, see Owning a Japanese home while living abroad for the 20.42% withholding on rent and for Tax Representatives.

Q3. What Are the 5 Methods for Non-Residents to Sell Japanese Real Estate?

⚠️ Important Note

There is no public statistical data on the breakdown of sale methods used by overseas sellers. The percentages below are SAMURAI's proprietary estimates based on insights from real estate industry practice, networks of buy-and-resell operators, and professional service networks.

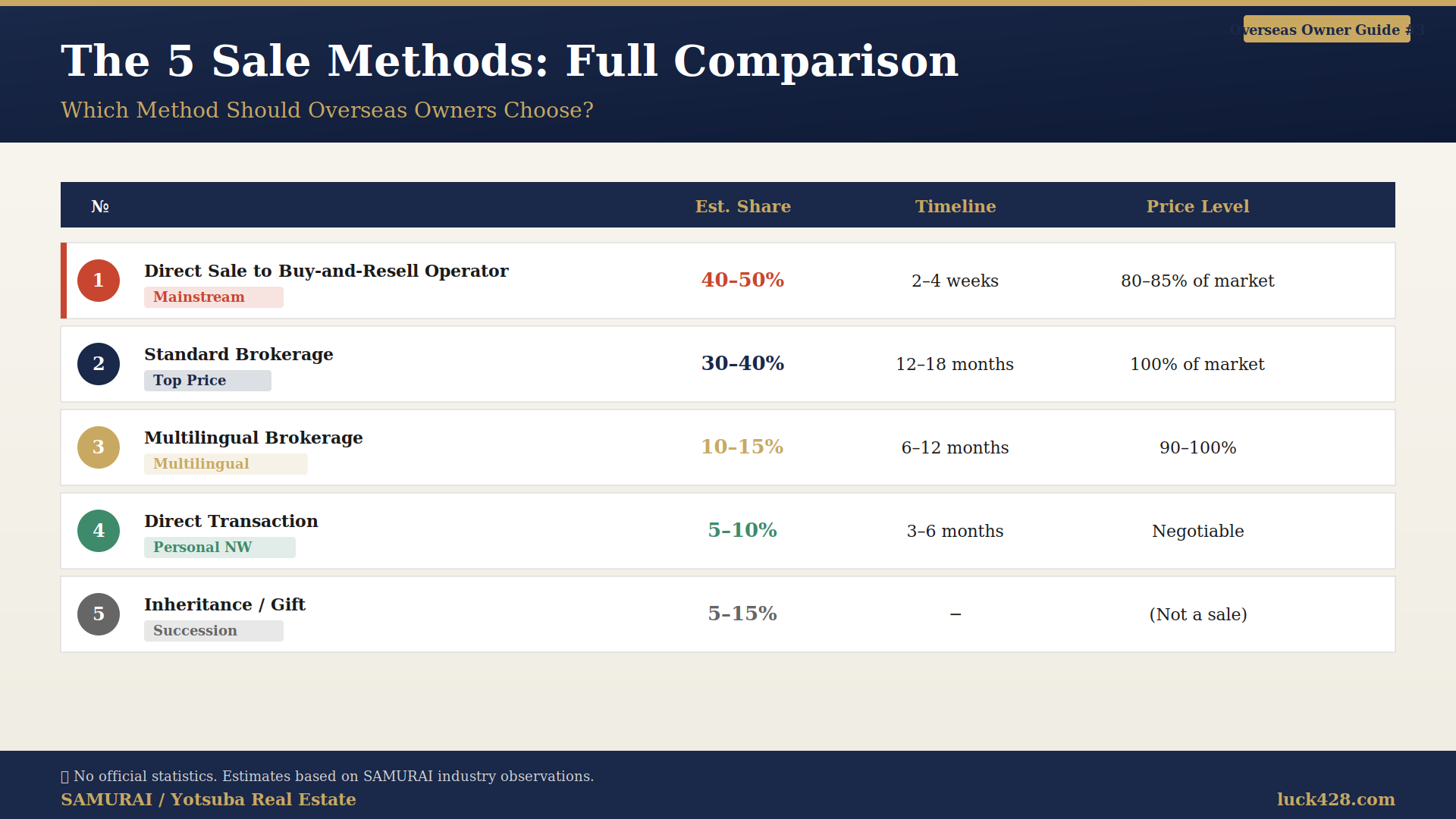

Comparison Overview of the 5 Methods

| Method | Estimated Share | Timeline | Price Level | Certainty |

|---|---|---|---|---|

| 1. Buy-and-resell operators | 40–50% | 2–4 weeks | 80–85% of market | ★★★★★ |

| 2. Standard brokerage | 30–40% | 12–18 months | 100% of market | ★★★ |

| 3. Multilingual brokerage | 10–15% | 6–12 months | 90–100% of market | ★★★★ |

| 4. Direct transaction | 5–10% | 3–6 months | Negotiable | ★★★ |

| 5. Inheritance/gift transfer | 5–15% | — | (Not a sale) | — |

Q4. What Is Method 1: "Direct Sale to a Professional Buy-and-Resell Operator"?

Estimated Share: 40–50% (Mainstream)

A buy-and-resell operator (a professional real estate company) acquires the property in cash on a quick-decision basis. For overseas owners, this is currently the mainstream choice as the fastest and most certain option.

Characteristics

- Contract to settlement in as little as 2–4 weeks

- Cash settlement (no mortgage approval; extremely low contract cancellation risk)

- Professional handling of 10.21% withholding tax procedures

- Reliable document handling (familiar with Signature Certificates, etc.)

- Capable of handling high-value properties exceeding 100 million yen

- No property viewings required (immediate buying decision after assessment)

Price Level

Typical buy prices: 80–85% of market value. Understand this slight discount as the price for speed and certainty.

Suitable Cases

- Need urgent liquidity (inheritance, return to home country, capital needs in home country)

- Want to delegate document handling to professionals

- Want to avoid the risk of prolonged sale via standard brokerage

- Want to avoid general buyers' resistance to handling withholding tax

- Older properties or properties with location challenges

Q5. What Is Method 2: "Sale via Standard Real Estate Brokerage"?

Estimated Share: 30–40%

Engaging a general real estate brokerage to find a buyer through the open market.

Characteristics

- Can target the highest market price

- However, settlement timeline tends to extend to 12–18 months

- General buyers often shy away from foreign sellers

- Individual buyers who dislike the withholding obligation tend to avoid such purchases

- Heavier burden of document preparation

Suitable Cases

- You have time and want to extract the highest price

- Premium properties in popular areas where buyers can be found relatively easily

- Sale price ≤100 million yen, with expected owner-occupier buyers (no withholding required)

⚠️ Important Caution

Many brokerages do not handle non-resident sales. Confirm in advance whether the brokerage has experience with non-resident transactions. Inexperienced brokers risk causing contract cancellation immediately before settlement due to documentation issues.

Q6. What Is Method 3: "Sale via Multilingual / Foreign-Capital Brokerages"?

Estimated Share: 10–15%

Selling through brokerages specialized in handling foreign clients, such as Plaza Homes, Re/Max, and Christie's International Real Estate.

Characteristics

- Multilingual support (Chinese, English, etc.)

- Strong access to overseas buyers (other overseas investors)

- Robust support framework for tax and documentation matters

- Brokerage commissions tend to be higher than standard (3.5–5%)

- Settlement timeline typically 6–12 months

Suitable Cases

- You wish to sell to overseas buyers

- You prioritize multilingual communication

- Premium properties in central Tokyo that can attract overseas high-net-worth individuals

Q7. What Is Method 4: "Direct Transactions Between Foreigners / Personal Networks"?

Estimated Share: 5–10%

Direct transactions among overseas owners through Taiwan investor networks, Greater China social media (Facebook groups, LINE, WeChat, Xiaohongshu), or personal introductions.

Characteristics

- May save on brokerage commissions

- Cultural understanding tends to be easier between foreigners

- When a non-resident acquires from another non-resident, FEFTA acquisition reporting is not required

- However, the seller still needs to handle withholding and tax filing

- Price levels vary significantly through negotiation

Suitable Cases

- A trustworthy buyer candidate exists within your personal network

- Property types where Greater China networks are active (central Tokyo condominiums)

- Privacy-focused transactions

⚠️ Caution

Even in direct transactions, document procedures (judicial scriveners, licensed real estate brokers) and tax procedures (withholding, tax filing) remain necessary as usual. Professional support is recommended to prevent disputes.

Q8. What Is Method 5: "Transfer via Inheritance / Gift"?

Estimated Share: 5–15%

Strictly speaking, this is not a "sale," but it is one of the major routes by which overseas owners part with Japanese real estate. It is often considered as an alternative to, or prior to, selling.

Characteristics

- Not a sale, but a transfer of ownership to family or relatives

- Gift tax or inheritance tax applies (with certain exemptions)

- Inheritance registration became mandatory from April 2024 (within 3 years of becoming aware of acquisition; up to 100,000 yen administrative fine for non-compliance)

- International inheritance requires complex tax coordination

- Family trusts allow staged succession during one's lifetime

Suitable Cases

- You wish to pass on Japanese real estate to children or relatives

- You wish to plan succession as part of future inheritance strategy

- You prefer continued family ownership over selling

- You wish to optimize taxes

Q9. Which Method Is Optimal for You? A Selection Framework

Recommended Methods by Priority

| Your Priority | Recommended Method | Reason |

|---|---|---|

| Speed-First (liquidity within 1–3 months) | Method 1 (Buy-and-resell) | Settlement possible in as little as 2–4 weeks |

| Price-First (highest price even if it takes time) | Method 2 or 3 (Brokerage) | Can target the highest market price |

| Certainty-First (avoid contract cancellation risk) | Method 1 (Buy-and-resell) | Cash settlement minimizes cancellation risk |

| Family succession included | Method 5 (Inheritance/gift) | Tax optimization possible |

| Privacy-focused | Method 4 (Direct transaction) | Matching through trusted network |

Q10. What Are the Key Considerations Before Selling?

Consideration 1: Tax Optimization Through Sale Timing

Capital gains tax rates differ by approximately 2x between holdings of ≤5 years and >5 years (short-term 30.63% vs. long-term 15.315%, both as non-resident income tax rates).

The criterion is whether the holding period exceeds 5 years as of January 1 of the sale year — so a sale on or after January 1 of the sixth year following acquisition is most favorable in tax terms.

Furthermore, if sold within 3 years and 10 months after inheritance, the inheritance tax acquisition cost addition special exemption may apply (NTA No. 3267) — an important exemption that reduces capital gains.

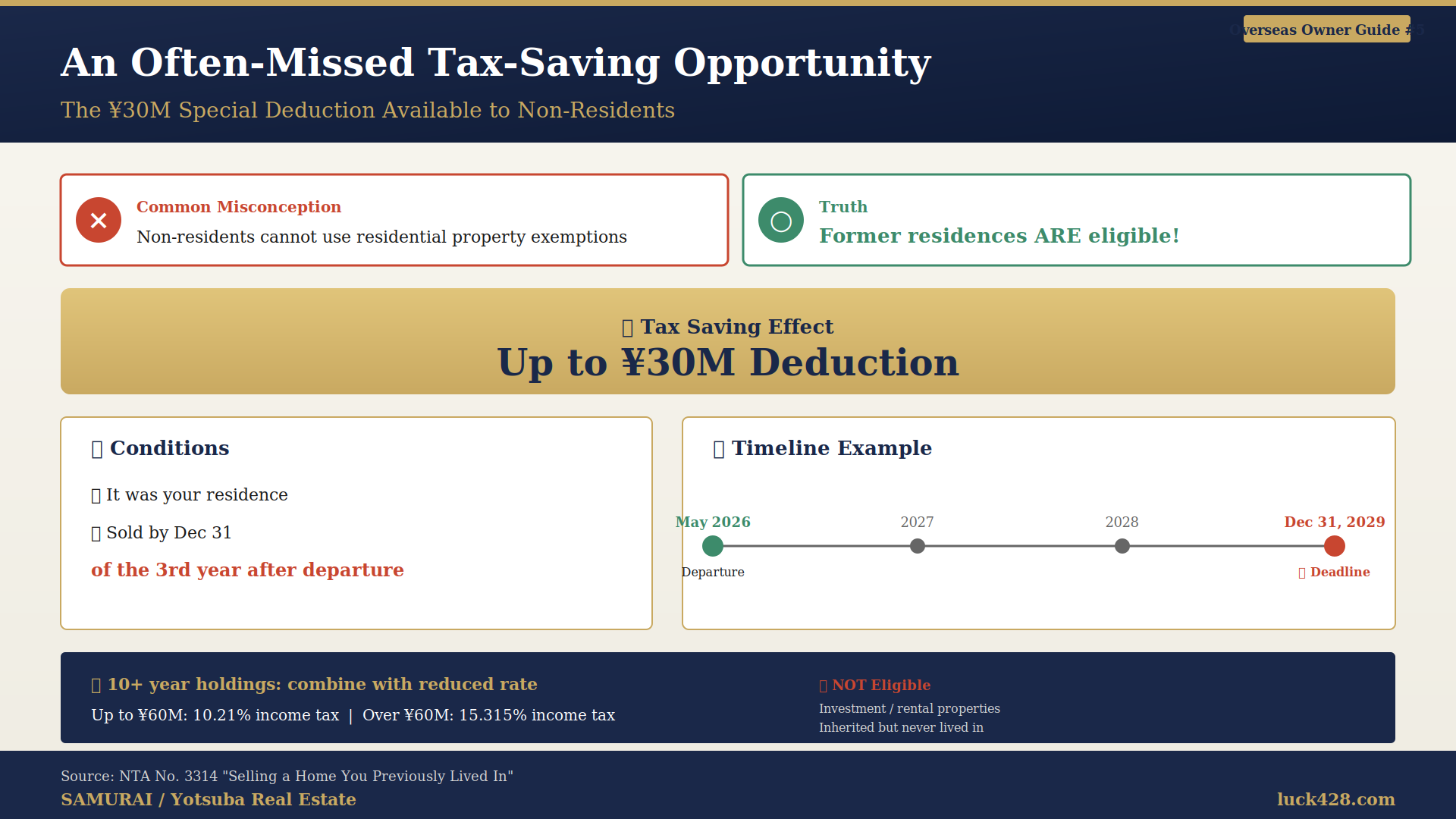

Consideration 2: Potential Application of the 30-Million-Yen Special Deduction and Reduced Tax Rate

The misconception that "non-residents cannot use the residential property special exemption" is common, but this is not accurate.

If you sell a home you previously lived in yourself after relocating or being assigned overseas, the 30-million-yen special deduction may apply if certain conditions are met (NTA No. 3314).

Application Conditions:

- The home was owned and lived in by you

- Sold by December 31 of the third year after the date you ceased to live there

Example: A person who left Japan in May 2026 selling their former home — sale by December 31, 2029 may qualify.

Combined Reduced Tax Rate (for properties held over 10 years):

| Taxable Capital Gains | Reduced Rate (Non-Residents) |

|---|---|

| Up to 60 million yen | 10.21% income tax |

| Portion exceeding 60 million yen | 15.315% income tax |

(Resident tax portion is generally not levied on non-residents.)

Properties NOT eligible:

- Originally purchased for investment/rental use

- Acquired through inheritance and never lived in

This represents a significant tax-saving opportunity, so we recommend planned sale considerations starting before departure, keeping the December 31 deadline (3 years after departure) in mind.

Consideration 3: Pre-Sale Renovation Strategy

When choosing standard brokerage (Method 2), pre-sale renovation can raise the price. However, when going through a buy-and-resell operator (Method 1), the operator presupposes renovation and resale, so seller-side renovation is unnecessary (and would be wasted).

Consideration 4: Currency Exchange Risk

Sale proceeds are received in Japanese yen. When converting to your home currency, exchange rate fluctuations have a major impact.

- Strong yen: Favorable for selling

- Weak yen: Unfavorable for selling

A judgment combining the review of long-term holding strategy with observation of currency trends is essential.

Consideration 5: Alternatives to Selling

Before rushing to sell, consider these alternatives:

- Rental management outsourcing (using management services for overseas-resident owners)

- Reverse mortgage or real estate-secured loans (when funding is needed)

- Family trust for staged ownership transfer

- Partial sale (transfer of a portion of co-ownership)

Q11. What Is the April 2026 FEFTA Ministerial Ordinance Amendment?

Overview of the Amendment

Effective April 1, 2026, an amendment to a ministerial ordinance under the Foreign Exchange and Foreign Trade Act (FEFTA) will require all non-resident transactions — including residential-purpose acquisitions previously exempt from reporting — to be subject to 20-day post-transaction reporting.

Before vs. After Comparison

| Item | Before | After (April 1, 2026 onward) |

|---|---|---|

| Investment-purpose acquisition | Reporting required | Reporting required |

| Residential-purpose acquisition | Not required | Required |

| Office-purpose acquisition | Not required | Required |

| Reporting deadline | Within 20 days of acquisition | Same |

| Submission destination | Minister of Finance via Bank of Japan | Same |

| Penalty | Administrative fine up to 500,000 yen | Same |

Implications for Sellers

The reporting obligation at the time of sale remains unchanged. However, since the buyer's reporting obligation expanded (in non-resident-to-non-resident sales), sellers should also be aware of their counterparty's reporting obligation.

❓ Frequently Asked Questions

Q. Can non-residents use the housing loan tax credit?

A. No. Non-residents cannot use the housing loan tax credit because they do not have living establishment in Japan.

Q. If I sell a Japanese condominium I purchased as a vacation home from overseas, will the withholding tax still apply?

A. Yes, in principle, the 10.21% withholding tax applies. It is exempted only if the conditions (sale price ≤100 million yen + individual buyer for residential use) are met.

Q. What happens if I do not file a tax return?

A. You may not be able to receive a refund of overpayments made through withholding. You also cannot offset losses if there is a capital loss. Tax filing is strongly recommended.

Q. How is the 100-million-yen threshold for withholding determined for co-ownership?

A. It is determined by each co-ownership share. For example, in a 50/50 co-ownership of a 150 million yen property, each share is 75 million yen — both below 100 million yen.

Q. Does the property tax adjustment payment count toward withholding?

A. Yes, property tax adjustment payments are considered part of the sale price, so the 100-million-yen threshold is determined based on the combined total.

Q. Can sale proceeds be remitted to my overseas bank account?

A. Yes. However, the amount remitted is after withholding. You should also factor in foreign exchange fees when calculating the actual amount.

Q. Are there special rules for selling to family members?

A. Sales to "specially related persons" — such as parents, children, spouses, or relatives sharing the same household — are not eligible for the 30-million-yen special deduction or the reduced tax rate exemption.

SAMURAI / Yotsuba Real Estate's Support for Overseas Owners

We at SAMURAI set out which professional handles which procedure, so that overseas owners can make optimal choices when the time comes.

The Representative's Expertise

- Former Bureau Chief, Mainichi Shimbun China Bureau (3 years stationed in Beijing; studied at National Taiwan Normal University)

- Triple-licensed: Administrative Scrivener, Labor and Social Security Attorney, Licensed Real Estate Broker

- Native-level proficiency in Chinese (both Traditional and Simplified)

One-Stop Service Offerings

| Service | Details |

|---|---|

| Sale method comparison & selection consultation | All 5 methods supported |

| Buy-and-resell operator network | Highest valuation from multiple operators |

| Buyer-side brokerage | Via Taiwan investor and Greater China networks |

| Tax Representative service | Administrative Scrivener serves directly |

| Tax return filing support | In coordination with SAMURAI tax accountant network |

| Inheritance registration & estate division | SAMURAI judicial scrivener and administrative scrivener network |

| International inheritance handling | Tax accountant and attorney network |

| FEFTA acquisition and sale reporting | Full handling |

| Multi-language support | Japanese, English, Traditional Chinese, Simplified Chinese |

Free Consultation

There is no need to rush to sell. As "knowledge for when the time comes," and to organize your future options, please feel free to consult us first — at no charge.

| Channel | Details |

|---|---|

| LINE | uramatsujoji |

| Facebook Messenger | facebook.com/uramatsujoji |

| uramatsujoji@luck428.com | |

| Website | luck428.com (4-language support) |

Closing: Holding for the Long Term, Yet Having Options

Japanese real estate is an extremely important asset for overseas owners — providing long-term stability of asset value, the function of preserving value as a yen-denominated asset, and preparation for the future of your family.

That many of you hold with the long-term in mind is, we believe, an extraordinarily sound investment philosophy. Rather than pursuing profits through short-term trading, the choice to continue holding assets with a long-term perspective often results in maximizing asset value — a fact also reflected in market data.

Yet, life brings unexpected turning points.

When that moment comes, whether or not you know your options will determine whether you can make the best decision.

We hope this column serves as "knowledge for when the time comes" for our overseas owner readers.

📚 Data Sources and Notes

- Japan Ministry of Land, Infrastructure, Transport and Tourism (MLIT), "Survey Results on New Condominium Transactions Using Real Estate Registration Information" (Published November 25, 2025)

- Japan Ministry of Finance, "Reporting Concerning Acquisition of Real Estate in Japan by Non-Residents" (Ministerial Ordinance under FEFTA, amended and effective April 1, 2026)

- Japan National Tax Agency (NTA):

- No. 1932: Selling Real Estate While Working Overseas

- No. 2879: Purchasing Land from Non-Residents

- No. 3314: Selling a Home You Previously Lived In

- No. 3267: Acquisition Cost Special Exemption When Selling Inherited Property

- The percentages for sale methods are estimates based on insights SAMURAI has gained from industry practice, buy-and-resell operator networks, and professional service networks. They are not official statistical data.

- This column is based on information as of May 2026. Tax laws and regulations are subject to amendment, and applicable tax rates and exemptions may differ depending on individual circumstances. We recommend consulting with a tax accountant or other professional when actually considering a sale.

Author: Joji Uramatsu

Affiliations: Representative Director, Yotsuba Real Estate Co., Ltd. / Principal Administrative Scrivener, Yotsuba Administrative Scrivener Office / Operator, Shigyo.com SAMURAI

First Published: May 8, 2026

Last Updated: May 8, 2026

🔗 Related Links

Related Articles

- 2026.07.28Commercial Spaces and Licensing

Health Department Requirements to Verify Before Signing a Takeover Property Agreement – Avoiding "We Signed the Contract, But Permission Was Denied"

- 2026.07.28Inherited Vacant Properties

Selling an Inherited Vacant Home with the 30-Million-Yen Deduction: Counting Back from 31 December of Year Three

- 2026.07.25本帰国

Ten Moves for Overseas Postings and Returns — What Helped Most, and a Real Estate Agent in Bangkok

Feel free to reach out for a consultation

Questions about our column articles are also welcome.